7 Smart Saving Strategies for Young Adults

Young adults can kickstart their financial future with these smart saving strategies. Begin by creating a budget using the 50/30/20 rule, allocating funds wisely between needs, wants, and savings. Set up an emergency fund to cover 3-6 months of living expenses for peace of mind. Use cash instead of credit to keep spending in check and reduce impulse buys. It's also essential to establish clear financial goals that are SMART: Specific, Measurable, Achievable, Relevant, and Time-bound. Finally, invest in your financial literacy through courses and resources, empowering you to make informed decisions. There's more to discover, so keep exploring!

Key Takeaways

- Establish a budget using the 50/30/20 rule to effectively allocate income towards needs, wants, and savings.

- Create an emergency fund with 3-6 months' worth of living expenses to prepare for unexpected financial challenges.

- Utilize cash for transactions to minimize impulse buys and prevent credit card debt, promoting better financial discipline.

- Set SMART financial goals to enhance focus and track progress towards achieving short-term and long-term savings objectives.

- Invest in personal finance education through courses, books, and resources to improve financial literacy and decision-making skills.

Learn How to Budget

Mastering the art of budgeting is fundamental for young adults looking to take control of their finances. Start by establishing a budgeting plan that categorizes your expenses into needs (50%), wants (30%), and savings (20%). This balanced approach helps you manage your budget effectively. Utilize budgeting tools or apps to track all your expenditures; this way, you can identify spending habits and discover areas for potential savings.

Regularly review and adjust your budget to reflect any changes in your financial situation. This guarantees you're on track to meet your financial goals and adapt to any unforeseen circumstances. Aim to allocate a specific percentage of your income each month for savings or investments, which is essential for building long-term financial stability.

Adhering to your budget is crucial for preventing expenses from exceeding your income, which can lead to unnecessary debt and financial stress. By committing to these practices, you empower yourself with the skills needed for effective financial management. Remember, budgeting isn't just about restriction; it's a pathway to achieving your savings goals and enjoying the freedom that comes with financial independence.

Create an Emergency Fund

After establishing a solid budgeting plan, the next step is to create an emergency fund. This fund is your financial safety net, ideally containing 3-6 months' worth of living expenses. By setting aside money for unexpected expenses, you can navigate life's uncertainties without adding financial stress.

To build your emergency fund effectively, consider these strategies:

- Open a high-yield savings account for better interest rates, allowing your money to grow while remaining accessible.

- Contribute a fixed percentage of your monthly income—even if it's just 1%—to develop the habit of regularly saving.

- Avoid tapping into your fund for non-emergencies; this reserve is for genuine financial surprises like medical emergencies or job loss.

- Aim for peace of mind, knowing you're prepared for life's unexpected twists.

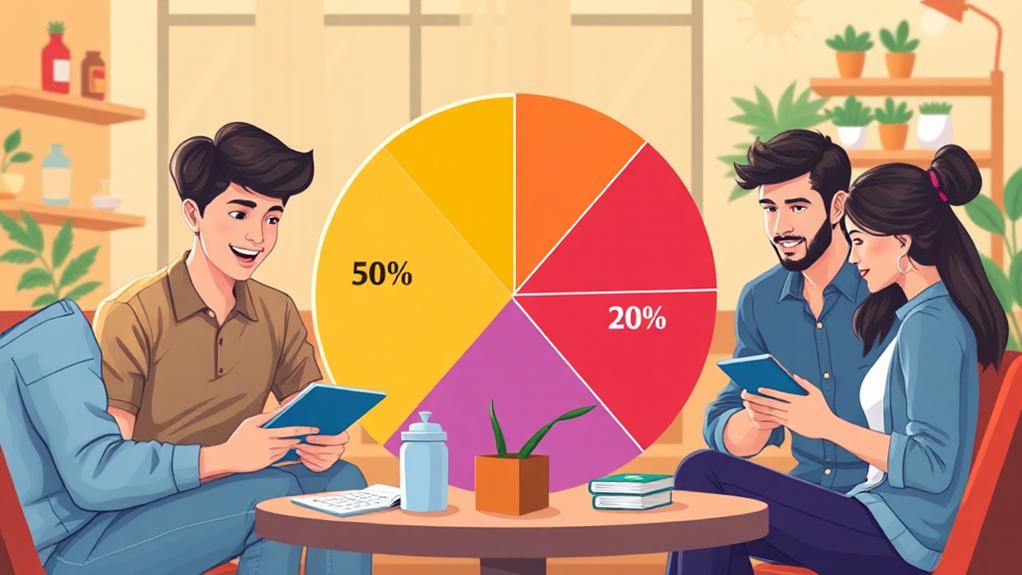

Use the 50/30/20 Rule

One effective budgeting method that can considerably simplify your financial management is the 50/30/20 rule. This straightforward approach allocates 50% of your income to needs—those essential expenses you can't avoid—30% to wants, which are your discretionary spending, and 20% to savings and debt repayment. By following this framework, you can develop healthier spending habits while ensuring your financial plan remains balanced.

For young adults, this method offers a clear path to financial stability. You'll find it easier to track where your money goes and prioritize your goals, whether that's building an emergency fund, saving for retirement, or tackling debt. Plus, knowing that your essential needs are covered can considerably reduce financial stress, allowing you to enjoy life while still preparing for the future.

Regularly reviewing and adjusting your budget according to the 50/30/20 rule helps you adapt to changes in income or expenses, keeping you on track. Embrace this simple yet effective strategy, and you'll cultivate consistent savings while enjoying the freedom that comes from smart budgeting.

Separate Needs From Wants

Separating needs from wants is a fundamental skill for effective budgeting and financial planning. When you identify what's essential versus what's a luxury, you can make smarter decisions about where your money goes. This clarity not only helps with saving money but aligns your spending with your financial goals.

Consider these categories:

- Needs: Housing, food, healthcare, transportation

- Wants: Dining out, entertainment, luxury items, subscriptions

- Savings: Emergency fund, retirement, investments, future goals

- Expenses: Fixed costs, variable costs, discretionary spending

By regularly reassessing your needs and wants, you can adapt your budget to fit your changing life circumstances. Implementing the 50/30/20 rule can guide you in allocating your income effectively—50% for needs, 30% for wants, and 20% for savings. This method guarantees that you prioritize paying for essentials while still enjoying a few of life's pleasures.

Invest in your financial education by using a budgeting app to track your expenses. Remember, distinguishing between needs and wants can lead to healthier financial habits and give you the freedom to achieve your financial dreams.

Use Cash Instead of Credit

Recognizing the difference between needs and wants sets the stage for smarter financial choices, and using cash instead of credit is a powerful way to reinforce that mindset. When you make cash transactions, you naturally engage in mindful spending. This method limits your purchases to what you can afford at that moment, helping you avoid impulse buys.

By avoiding using a credit card, you eliminate the risk of accruing interest and debt, which can lead to financial strain. Studies show that individuals who use cash spend about 20% less than those who rely on credit, highlighting how effective cash can be in controlling expenses.

Using cash also improves your budgeting skills, as it gives you a tangible way to track spending in each category. This clarity makes it easier to stick to your budget. Moreover, relying on cash fosters better financial discipline, requiring you to plan and prioritize your spending.

Incorporating cash into your financial routine can lead to healthier financial habits and ultimately improve your financial situation. Start implementing these saving tips today, and you'll gain the freedom that comes with financial control.

Set Financial Goals

Setting financial goals is essential for charting your path to financial success. When you set financial goals, you create a clear roadmap that keeps you focused on what truly matters. Using the SMART criteria is key: make your goals Specific, Measurable, Achievable, Relevant, and Time-bound. This approach not only clarifies your objectives but also boosts your motivation to track progress.

Consider setting both short-term and long-term goals to enhance your financial health. Here are some examples to inspire you:

- Saving for a car in the next two years

- Building an emergency fund that covers three to six months of expenses

- Contributing regularly to retirement savings for long-term stability

- Aiming to pay off student loans within a certain timeframe

Research shows that writing down these goals can increase your likelihood of achieving them by up to 42%. Regularly reviewing and adjusting your goals guarantees you adapt to changing circumstances, reinforcing your accountability. By setting financial goals, you empower yourself to take control of your finances and work towards the freedom you desire.

Educate and Invest in Yourself

Investing in yourself is one of the smartest moves you can make for your financial future. By prioritizing education, you enhance your financial literacy and improve your decision-making skills. Consider enrolling in personal finance courses or obtaining certifications; these can lead to higher earnings over your lifetime.

Self-education is key—read personal finance books and follow financial blogs to uncover valuable strategies. Studies show that those who invest in their financial knowledge tend to experience better outcomes and lower debt levels.

Networking with professionals in your field can also open doors to mentorship and career advancement opportunities, essential for achieving financial success. Don't overlook the wealth of free online resources available for skill development; staying competitive in the job market can greatly boost your income and financial stability.